Despite a surge in PE fundraising in the latter part of the year, many fund managers chose to delay their fundraising efforts due to broader market conditions over the past year

Indeed, 2023 marked the most challenging year in private markets in nearly a decade, with a significant slowdown in fundraising activity

Nonetheless, there will be successful players as capital is still available for funds with clear strategies who use new technology to help them stay ahead of the competition

The industry wide “retailization” trend, and moves to improve transparency, will allow new entrants in private markets investing, increasing the available capital to fund managers

Much has been said about the fundraising slowdown across private markets last year. Despite this, it appears that the fundraising market is on the brink of resurgence, indicating growing demand. Therefore, it’s crucial to act now, align your efforts, and stay ahead of the competition to avoid falling behind.

Reflecting on the past year, raising capital in 2023 became increasingly challenging, supported by disappointing fundraising data. However, what do the numbers truly signify, and was capital readily available last year for investment firms with clear visions and compelling strategies? Additionally, did any asset class thrive in 2023? In our latest insights article, we delve deep into last year’s multifaceted private market fundraising sector, exploring these questions and more.

The enduring resilience of private equity

We have previously spoken about the enduring resilience of private equity throughout downturns and this was evident in Q4 of last year[1]. Private equity deal value increased by over 58% compared to Q3, marking a 20% increase compared to Q4 2022 and the highest quarter in the last six quarters.

Despite these promising indicators, private equity deal volume declined in both Europe (13.6%) and North America (6.4%), indicating that the asset class was not immune to the fundraising downturn. However, as interest rates stabilize and major global economies evade previously forecasted recessions (for now), private equity continues to demonstrate its resilience across economic cycles.

2023 recap: Fundraising slows before year-end optimism

Global conflicts, political instability and rising inflation rates contributed to a challenging economic climate last year, with the private markets being no exception. This further filtered down to fundraising facing its toughest year in almost a decade. Capital raised decreased, and fewer funds reached a first close. Yet, the last quarter of the year showed promise for private market fundraising, with private equity already demonstrating its resilience during uncertain times. Let us examine the 2023 data.

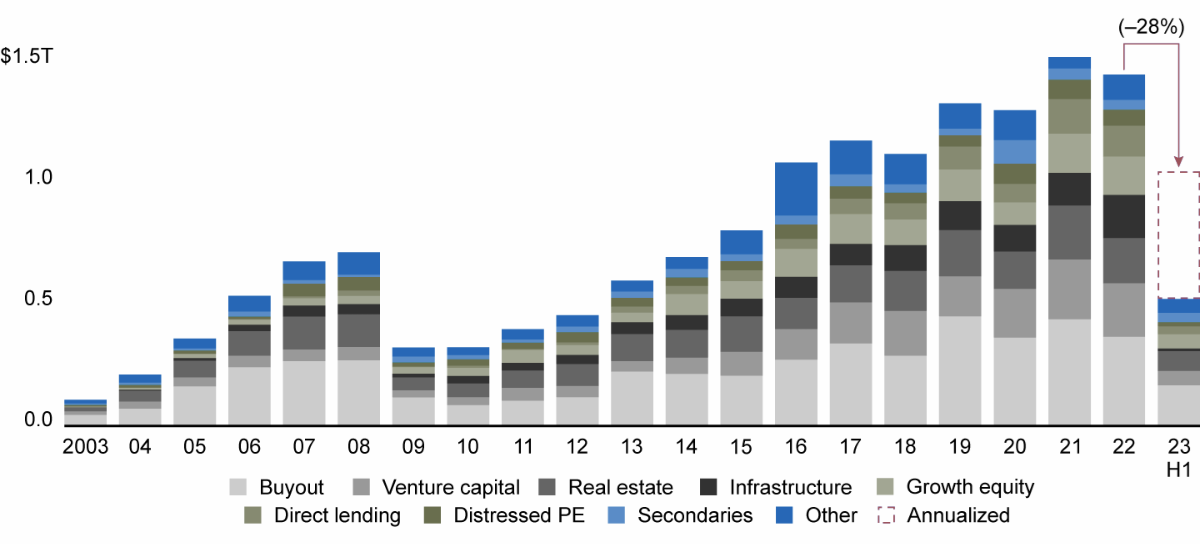

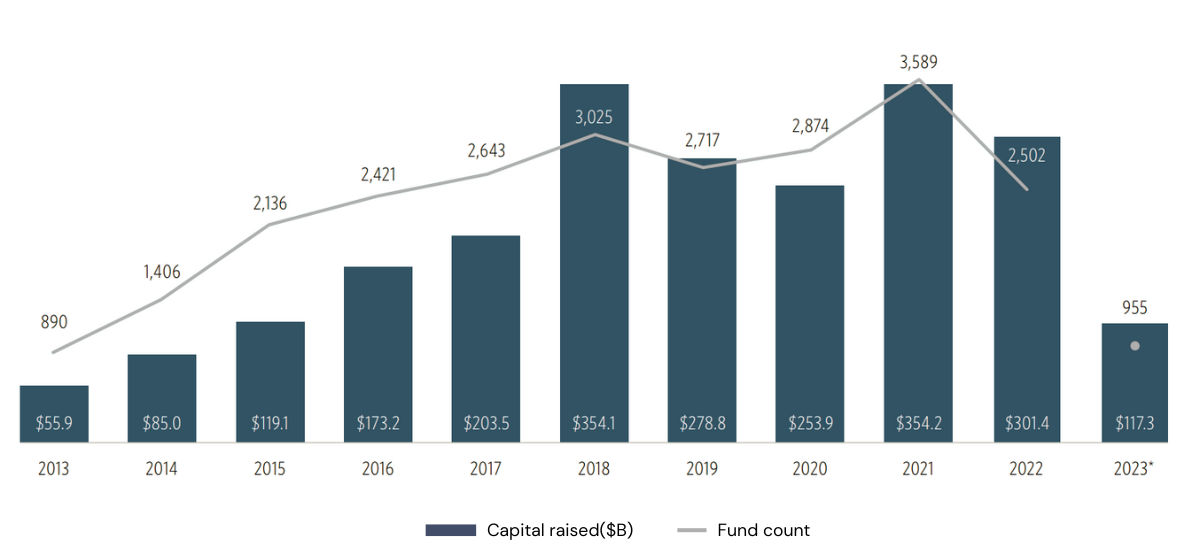

By midyear, it was evident that fundraising had significantly declined. As highlighted in the below graph[2], global private capital raised in the first six months fell to $517 billion. A 35% decline compared to the same period in 2022, with a 28% decrease predicted at year-end.

Figure 1: Global private capital raised

Source: Preqin. Notes: Buyout includes buyout, balanced, co-investment, and co-investment multimanagers; includes funds with final close and represents the year in which they held their final close; excludes Softbank Vision Fund; other includes fund of funds, mezzanine, hybrid, hybrid credit strategies, real asset, private investment in public equity (PIPE), collateralized loan obligation (CLO) funds; excludes natural resources

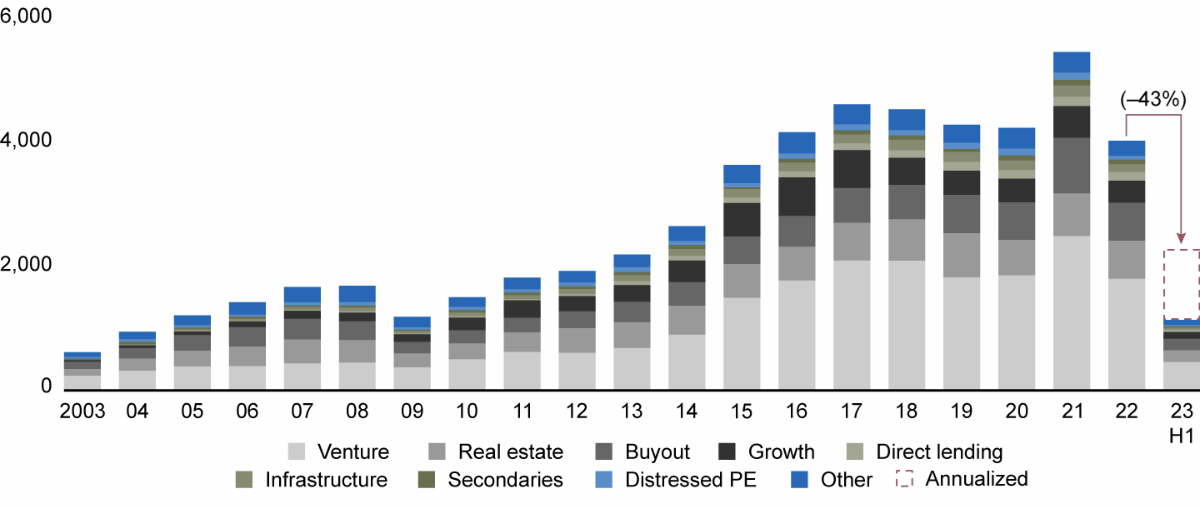

From the same mid-year data, the second graph[3] below illustrates a significant decrease in private market funds closing. The level of which we have not seen in almost a decade. A 43% decrease in funds closing was predicted at year-end.

Figure 2: Global private credit raised, by count of funds

Source: Preqin. Notes: Buyout includes buyout, balanced, co-investment, and co-investment multimanagers; includes funds with final close and represents the year in which they held their final close; excludes Softbank Vision Fund; other includes fund of funds, mezzanine, hybrid, hybrid credit strategies, real asset, private investment in public equity (PIPE), collateralized loan obligation (CLO) funds; excludes natural resources

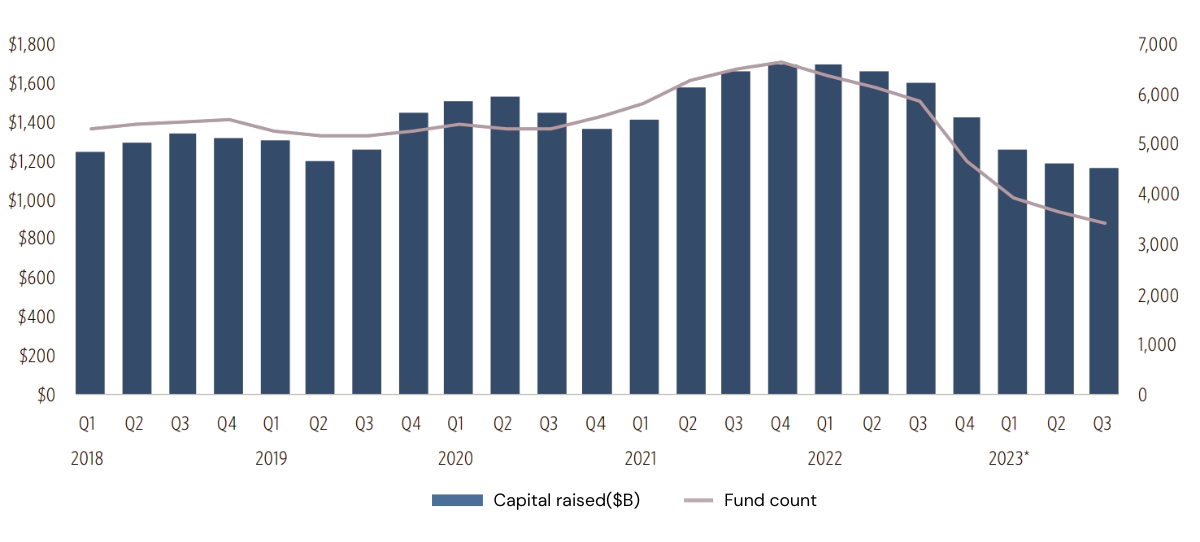

Pitchbook data[4] from the third quarter of 2023 confirms the general sentiment that private markets fundraising remained challenging in the second half of the year. The below graph indicates how overall private capital raised in Q3 decreased by approximately 14% compared to the previous year.

Figure 3: Rolling 12-month private capital fundraising activity

As widely reported, the fundraising climate in venture capital (VC) remains particularly tough, with a massive drop in VC fundraising highlighted in the next chart[5].

Figure 4: VC fundraising activities

Source: Pitchbook Geography: Global

* As of September 30, 2023

This decline is largely attributed to the continued perception of inflated valuations of early-stage tech companies prompting investors and Limited Partners (LPs) to adopt a more cautious approach. Notable examples, such as the sky-high valuation of WeWork leading to its eventual downfall, have understandably influenced LP’s mindset when valuing early-stage tech companies lacking a proven business model or evidence of significant market traction. Unfortunately, this trend persisted into the final quarter of the year, with only half the number of exits compared with Q4 2022, signaling a prevailing negative sentiment in early-stage investing[6]. On the fundraising front, 174 VC funds closed in the quarter, marking a 30% decrease from Q3 2023 and a 5.5% decline in value.

Nevertheless, with lower interest rates and a predicted resurgence of the global IPO market in 2024, we anticipate a significant increase in VC fundraising. Brighter times are ahead.

On a more positive note, secondary funds enjoyed their time in the sun last year[7]. These funds achieved a record 8.6% share of fundraising in the third quarter of 2023 as an increasing number of continuation vehicles launched. This strategic move enables fund managers / General Partners (GPs) to delay exits for more favorable market conditions expected in the future.

“Capital is still available for compelling funds with clear strategies.”

Despite the overall negative sentiment surrounding fundraising this year, over 3,400 funds successfully closed in 2023. This shows us that capital is still available for compelling funds with clear strategies.

But the market dynamics mentioned above are causing many firms to delay or reassess their fundraising ambitions. Coupled with record levels of dry powder, allowing fund managers extra time for valuations to adjust before committing their capital. For instance, at $108B, European venture funds continue to sit on the largest amount of deployable capital the region has ever seen[8].

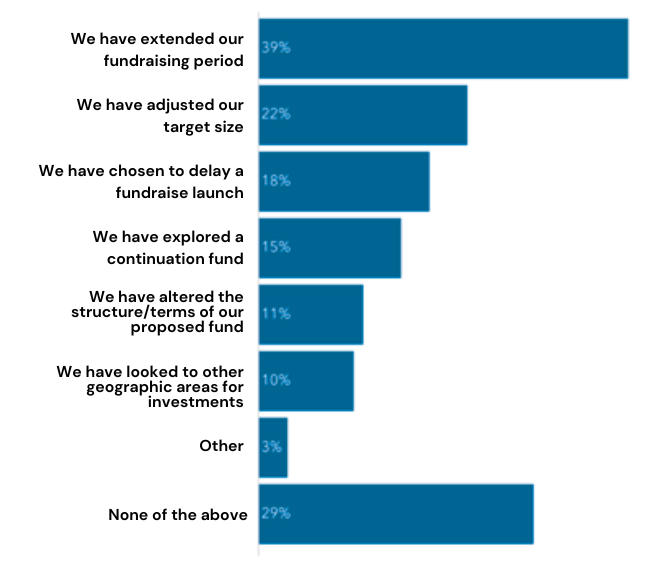

Figure 5: How have the recent market conditions impacted fundraising efforts?

According to a recent Private Funds CFO survey[9], over two-thirds of finance leaders reported that finding new investors is either ‘challenging’ or ‘extremely challenging’ in the current climate.

Additionally, 39% decided to extend their fundraising period, with 18% opting to delay a fundraise launch altogether (see full survey answer on the left).

Percentages have been rounded

Source: Private Funds CFO Insights Survey 2024

Embracing technology

The current market conditions have caused a fundraising environment where the number of fund managers seeking capital exceeds the available funding. Research by Preqin[10] reveals approximately 14,000 active funds competing for $3.3 trillion of capital, while only about $1 trillion is available.

While we are confident the fundraising market will inevitably pick up again, GPs can use this time wisely, adopting innovative approaches to remain successful. Technology holds the key with an increasing number of GPs now realizing that new digital solutions must be utilized to stay ahead of the competition.

“Fund managers can use this time wisely, adopting innovative approaches to remain successful.”

Even though there has been an uptake throughout the private markets in utilizing new technological solutions to streamline operations, fundraising has often lagged. The global Covid-19 pandemic and enforced working from home policy for most, gave both investors and fund managers the confidence in raising and investing capital remotely with the right digital tools. This is why we launched Bite Stream globally; an end-to-end Software-as-a-Service (SaaS) investor management and fundraising platform designed with both the user experience of investors and fund managers in mind.

Another huge technological development this year is the rise of Artificial Intelligence (AI) which is already gaining traction throughout the private markets. Notably, leading global investment firm, EQT, have created their own AI-based ‘Motherbrain’ where they are harnessing the power of AI to identify deals earlier than previously possible [11]. The tool was initially designed for their venture capital team but has since been rolled out across their private equity and infrastructure teams.

It is no surprise to learn that this forward-thinking offering has proven popular with investors across the globe. Despite the tricky fundraising climate, the firm’s latest flagship fund is expected to close on €21.5 billion, 38% higher than its predecessor and significantly over the original €20 billion target[12].

Other examples of new AI-based software in the wider finance markets include the Bloomberg terminal which conducts analysis of company performance written by artificial intelligence[13]. It’s clear, investors harnessing AI-based solutions will only become more prevalent.

Still, as we found out in our 2023 The Tech’s Factor report[14], firms should be aware of learning to walk before they can run. The effective integration of AI requires a foundation built on existing technologies. Those who have not prioritized digitalization investments, such as transitioning to centralized cloud-based solutions and strategically planning their infrastructure, will struggle to unlock the full potential of AI.

Move to greater transparency opens new opportunities

In our previous article, we discussed how the new Securities and Exchange Commission (SEC) rules and regulations could have far-reaching consequences for the private markets. This is part of a clear industry-wide move towards becoming more transparent in response to the growth achieved since the turn of the century. With an increased scrutiny from an ever-growing investor base, GPs would be wise to utilize the technology solutions available in today’s market to provide greater transparency, significantly improving the direct communications and reporting metrics given to investors.

This will lower the barrier of entry into the private markets for first-time investors, in turn increasing the amount of capital circulating throughout the fundraising sector. An example of this could be enhancing wealth management channels with more advisors than ever before representing all types of investors who are aiming to tap into the massive investment opportunities on offer.

Conclusion

Fundraising in 2023 paints a mixed picture. Yes, there is no getting away from the fact of there being a slowdown in fundraising due to a challenging global economic climate, but it is not all doom and gloom. Private equity is already showing signs of a strong recovery and with further growth of private markets widely expected. Especially as new types of investors enter the scene. Capital will be available for the GPs that are committed to adopting new cutting-edge technologies, modernizing operations, increasing transparency, and communicating better with their investors. 2024 promises to be an exciting year for many!

Sources:

- Preqin, Private Equity Q4 2023: Preqin Quarterly Update, January 2024

- Bain & Company, Stuck in Place: Private Equity Midyear Report 2023, July 2023

- Pitchbook, Private Market Fundraising Report, December 2023

- Pitchbook, Private Market Fundraising Report, December 2023

- Pitchbook, Private Market Fundraising Report, December 2023

- Preqin, Venture Capital Q4 2023: Preqin Quarterly Update, January 202

- Pitchbook, Private Market Fundraising Report, December 2023

- Atomico, State of European Tech 2023 report, November 2023

- Private Funds CFO, Insights 2024: Fundraising hits hard times, December 2023

- Preqin, Private Equity Q4 2023: Preqin Quarterly Update, January 2024

- Private Equity International, EQT’s Alexandra Lutz: Motherbrain will be the “backbone of the investment lifecycle”, July 2022

- Private Equity International, EQT to close latest flagship on 21.5bn euro hard-cap, October 2023

- Institutional Investor, Bloomberg’s First Generative AI Tool Hits the Terminal, January 2024

- Bite Investments, The Tech’s Factor 2023: The digital (r)evolution in private markets, July 2023

Disclaimer: This article is made available by BITE Investments (UK) Limited (“Bite UK”), a company incorporated in the United Kingdom (company registration number 11706620) with its registered office at 28 Ecclestone Square, London SW1V 1NZ. The information contained in this article (the “Information”) is for informational purposes only and may not be relied upon for the purposes of evaluating the merits of investing in any shares, other securities, limited partnership interests or other interests in any funds listed or referred to in the article or for any other purpose. The Information does not constitute an offer to acquire any limited partnership interests, shares or other securities, make any investment or to provide any fund management services or any investment advice of any kind, nor does this article constitute an invitation to invest, directly or indirectly, in any company or collective investment scheme, or to undertake to do so. Reliance on the Information for the purpose of engaging in any investment activity may expose the investor to a significant risk of losing all of the money invested. Nothing in this article is to be construed, and shall not be relied upon as, legal, regulatory, credit, business, tax or accountancy advice. The Information may change and there shall be no obligation on the part of Bite UK to update any of the Information. Data and facts used in this article are derived from sources which are considered to be reliable and have been compiled using Bite UK’s best knowledge. However, Bite UK does not guarantee the correctness of the Information. This article and the Information are strictly confidential and are used exclusively for a limited number of addresses. Reproduction of this article or the dissemination of this article, or the Information, to third parties, is not permitted.

Learn more about how Bite Stream can help you

Discover a solution that suits your needs