A ‘Bite’ of Private Markets – delivering Facts, Insights & Strategies

Alternative Investments in the Mainstream

William Rudebeck

Chief Executive Officer

Overview

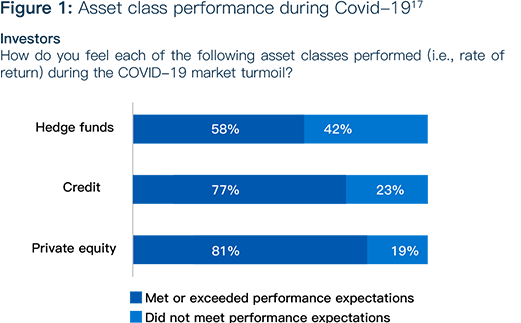

It is no longer a matter of if or when. Alternatives are now clearly in the mainstream. Despite the impact of a global pandemic, and during the height of market volatility in 2020, almost all alternative fund strategies significantly exceeded major benchmarks.[1] In fact, according to results from the 14th annual EY Global Alternative Fund Survey, investors indicated that their managers outperformed their performance expectations during Covid-19, especially in private equity, with a ratio of 4:1.[2] Old projections were for alternatives to grow from $13.6tn on the conservative side to $15.3tn on the high side by the close of 2020.[3] Based on data, forecasts are for alternatives to increase to $17tr in assets under management (AUM) by 2025.[4]

In 2021, the appeal of alternatives has not ebbed at all and continues to grow among institutional investors, high net worth (HNW), and ultra high net worth (UHNW) investors. Eighty one percent (81%) of UHNW investors, 55% of HNW investors and 14% of the mass affluent hold alternative investments, with UHNW investors (i.e., those with a minimum net worth of $30 million) estimated to have 50% of their assets, on average, allocated in alternatives.[5] According to KKR’s Family Office Survey, private equity held the largest allocations among the alternative asset classes at 54% in 2020. The same report shows that of the alternative asset classes, only private equity and real estate achieved portfolio growth for HNW families over the period from 2017 and 2020.[6]

Regarding the HNW and UHNW investor sector, wealth managers, eager to satisfy their clients’ increasing appetite for investments like private equity, too are ramping up their search for these investments and platforms that facilitate access and ease the due diligence process. There are other factors too that are driving the mainstreaming of alternatives. HNW and UNHW investors are seeking broader portfolio diversification along with investments that deliver real long-term alpha. They want higher returns and yields than what traditional investments have proven to give. Today’s low to zero interest rate environment has prompted many investors to broaden their portfolio strategies. This is particularly applicable to the Asia-Pacific region.

For Asia’s affluent investors, there are those who are specifically seeking higher returns, while others are looking for yield in combination with a lesser correlated alpha generation and risk mitigation. Regardless of their goals, Asia’s HNW and UHNW investors are demonstrating an increased demand for alternatives, in particular private equity, private credit, hedge funds, gold, and commercial real estate. A survey of independent wealth managers in Asia found that most favour allocations of between 10% and 30% in alternatives.[7] When asked – What key trends do you see amongst HNW and UNHW private clients in Asia in terms of demand for alternative investments? – these wealth managers cited a 91% increasing demand, and 9% seeing demand remaining the same.[8]

Within Asia, China is the primary driver of alternative investment growth. Greater China’s private equity and venture capital industry’s assets under management (AUM) represent 74% of capital targeting the broader Asia-Pacific region.[9]

Singapore is also proving a strong market for alternatives as well as traditional investments, with AUM projected to have risen 17% in 2020 based on data from the Monetary Authority of Singapore (MAS).[10] Within the alternatives category, strong inflows were recorded in private equity, real estate, REITs, and venture capital.

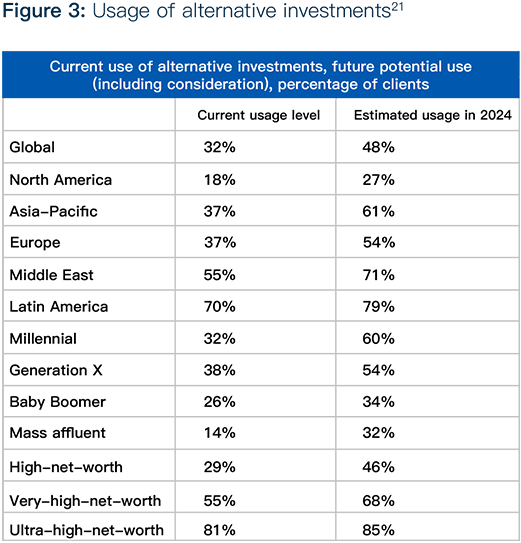

Overall, the current and projected use of alternatives varies from region to region. Latin American UHNW investors surveyed by EY have the highest percentage at 70% currently with projected growth to 79% by 2024; followed by investors in the Middle East at 55% currently using alternatives with a projected growth to 71% by 2024.[11]

While alternatives are mainstream and present significant opportunities for investors and advisors, capitalising on their growth and steadily increasing demand is not without its challenges.

Behind the Numbers

* From 2017 to 2023, private equity is projected to increase by 58%, going from $3.1tn to $4.9tn and private debt is expected to increase by 100% from $0.7tn to $1.4tn.[12]

* Many analysts expected global wealth to decrease due to the pandemic. However, instead of shrinking, global financial wealth soared, rising over 8.3% over the course of 2020 to reach an impressive all-time high of $250 trillion. Over the next five years, North America and Asia (excluding Japan) will be the leading financial wealth generators in absolute terms, followed by Western Europe.[13]

* A survey of HNW private investors conducted by the specialist private client investment business Connection Capital found that 87% plan to maintain or increase their allocations in alternative asset funds, 79% in private equity and 67% in private credit compared to 64% who indicate the same for the stock market.[14]

* Alternative investments under management in the Asia-Pacific region are projected to reach almost $5 trillion by 2025.[15] This would be coming from the $1.71 tr. in September 2020.[16]

Market Challenges

For a long time, alternative investments were largely confined to institutional investors who could withstand the high buy-ins with initial investments often as high as $10m plus for the best funds, as well as the long lock-up periods; sometimes a duration of 10 years. Now however, there are innovative, market-responsive companies that have effectively removed those barriers. Raising awareness regarding these new opportunities in alternatives with both the independent financial advisors (IFAs)/wealth managers and the clients is necessary.

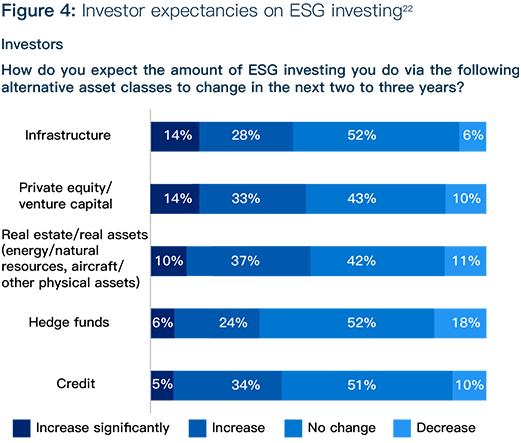

Investment advisors have cited their need for better pricing and a more defined strategy from the specialist managers they typically have used for alternative products. There is also the need for a selection of investments that reflects their clients’ value systems. These Environmental, Social and Governance (ESG) investments must be integrated into the alternative investment strategy offered to clients. Concurrent with this expectation is investors’ increased focus on their advisors’ own ESG and Diversity and Inclusion practices. While the primary objective of asset managers is to preserve and grow investor capital, managers are increasingly being asked by all constituents to do more as corporate citizens[19].

Digitalisation poses a necessary challenge that both investment advisors and alternative product specialists need to overcome. Given the number of well-designed and functional fintech platforms now available, it is important that those who are holding on to old practices and processes begin to accept that digital tools are necessary to remain competitive. This is especially true with the Great Wealth transfer underway as Baby Boomers begin transitioning their assets to their heirs and these digital natives expect digital access from their advisors. Further, it is not the Millennials and younger generations requiring digital access, but older HNW and UHNW investors also have this expectation, especially in the Asia-Pacific region[20]. There, investors regard using online platforms and mobile apps as part of a good advisor/client relationships and just as important as having in-person meetings.

In short, leveraging digitalisation will be critical for meeting client expectations, while achieving enhanced, automated processes that streamline operations, support due diligence, mitigate compliance-related risks, and facilitate a transition to a more future-proof business model. Financial advisors have the ability to use existing third-party fintech platforms focused on alternatives or have a bespoke solution developed to accommodate their practice needs.

Another challenge that must be addressed to succeed in capturing alternative investment opportunities is managing the associated risks and related reporting. In addition to expecting a level of customisation and performance, HNW and UHNW investors are demanding that risk limits be enforced. Advisors who are not aligned with this expectation are likely to suffer the consequences of fee reductions or terminations. Therefore, it is imperative that a sound risk management policy encompassing governance and performing benchmarking be in place. For some practices, establishing an independent risk officer and/or risk committee may be warranted.

Within certain markets, there may also be other obstacles to address such as regulatory changes. In many parts of the world, asset managers face hurdles in government interventions which introduce new risks and requirements that may be onerous for some practices. On the positive side, this often leads to more transparent financial systems. Additionally, measures such as eliminating guarantees for state-owned enterprise and local government financial vehicles have helped create a more market-driven financial system in many regions which benefits advisors and investors.

Market Opportunities

While the mainstreaming of alternatives is not without its growth pains, there is no denying the opportunities this trend has ushered in for investors and advisors alike. By introducing alternatives into their portfolios, investors have the opportunity to achieve their goals relating to increased diversification to mitigate market volatility, as well as to try to capture alpha, higher returns and yields.

Asset managers can support their goals of growing their AUM and meeting/exceeding client expectations. In their adoption of digital tools, offering of alternatives including those which reflect clients’ ESG investing objectives, along with establishing and communicating their own ESG policies, asset managers can position themselves for future growth and opportunity.

If industry consolidation does occur, as some are predicting in light of the pandemic fallout, those firms that have moved into the alternative arena in the best way possible – by aligning with alternative investment providers that offer both best in class investments, as well as digitised their operations and implemented robust fintech solutions – and vowing to educate their staff and clients regarding alternatives, they will likely be among the practices that remain and thrive.

Asset managers operating globally can capture new opportunities and expand their market reach where alternatives are especially in high demand.

Leveraging Alternative Investments and Private Market Technology Solutions

Bite Investments was conceived with a mission of enabling access to meaningful alternative investment opportunities that helped meet the goals of both the wealth management/independent financial advisor industry and their HNW and UHNW clients.

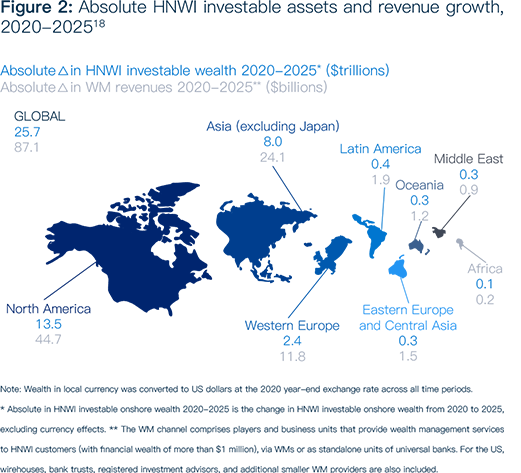

Personal financial wealth has soared over the past two decades with total global financial wealth reaching a record high of $250 trillion in 2020, according to BCG. They estimate that between now and 2025, $65 trillion of wealth will be generated, of which $25 trillion will come from North America, $22 trillion from Asia, and $10 trillion from Western Europe [23]. To cater to the global expansion of HNWI wealth, wealth managers are leaning towards alternative investment opportunities.

Today’s best-in-class fintech platforms offering alternatives feature a seamless, end-to-end investment process. At Bite Investments, our robust platform enables an account to be created, followed by log in to access the funds, due diligence to be performed and investments to be selected, and allocations to be requested for online investing, and finally, the signing of subscription documents. Thereafter, the investor can continually track and obtain updates to monitor the investments’ performance.

For advisors, asset & wealth managers, private banks, and fund managers digitising their operations, Bite provides private market technology strategies including turnkey white labelling options and bespoke technology solutions.

Bite’s specialist private market technology solution allows you to compliantly streamline your client onboarding and investment management process. Our technology platform automates the entire investment cycle from client suitability and distribution, through to subscription and reporting in a fully automated way.

Risk warning: Investment is restricted to professional, high net worth and sophisticated investors who can demonstrate that they have sufficient knowledge and experience to understand the risks of investing. Risks include the potential loss of capital and limited liquidity. Investments are long term and it may not be possible to sell your investment prior to maturity. Past returns are not a reliable indicator of future performance.

Disclaimer: All Rights Reserved. No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form by any means, electronic, mechanical, photocopying, recording or otherwise, without the prior permission of the publisher, Bite Investments. The facts of this fact sheet are believed to be correct at the time of publication but cannot be guaranteed. Please note that the findings, conclusions and recommendations that Bite Investments delivers are based on information gathered in good faith from both primary and secondary sources, whose accuracy we are not always in a position to guarantee. As such, Bite Investments, can accept no liability whatsoever for actions taken based on any information that may subsequently prove to be incorrect.

This document has been prepared purely for information purposes, and nothing in this report should be construed as an offer, or the solicitation of an offer, to buy or sell any security, product, service or investment.

[1] EY, “In times of change, does accelerated adaptation present obstacles or opportunities? 2020 Global Alternative Fund Survey”, Nov 2020

[2] EY, “In times of change, does accelerated adaptation present obstacles or opportunities? 2020 Global Alternative Fund Survey”, Nov 2020

[3] PwC, Market Research Centre analysis based on Preqin, HFR and Lipper data in “Alternative asset management 2020 – Fast forward to centre stage”, Jun 2015

[4] BNY Mellon, “From Alternative to Mainstream”, Jun 2021

[5] The Motley Fool, EY 2021 data in “81% of Ultra-High-Net-Worth Individuals Use Alternative Investments”, by Jack Caporal, 18 Aug 2021

[6] KKR, “The Wisdom of Compounding Capital”, by Henry H. McVey, 2 Feb 2021

[7] Hubbis, “In a World of Near-Term Uncertainty, Alternatives Move Centre Stage for Asia’s Wealthy, 9 Sept 2020

[8] Hubbis, “In a World of Near-Term Uncertainty, Alternatives Move Centre Stage for Asia’s Wealthy, 9 Sept 2020

[9] Bloomberg, Preqin data in “Alternative Assets in Asia Pacific May Near $5 Trillion in 2025”, by Alice Huang, 6 Jun 2021

[10] Asian Investor, “Assets under management in Singapore rises 17% to $3.5 trillion”, by Natalie Koh, 30 Jun 2021

[11] The Motley Fool, EY 2021 data in “81% of Ultra-High-Net-Worth Individuals Use Alternative Investments”, by Jack Caporal, 18 Aug 2021

[12] Preqin, “The Future of Alternatives – The Classes of 2023”, Nov 2018

[13] BCG , “When Clients Take the Lead – Global Wealth Survey 2021″, Jun 2021

[14] Wealth Adviser, Connection Capital survey data in “HNW investors gearing up for alternative investment opportunities”, 15 Jun 2020

[15] Bloomberg, Preqin data in “Alternative Assets in Asia Pacific May Near $5 Trillion in 2025”, by Alice Huang, 6 Jun 2021

[16] Wealth Briefing Asia, Preqin data in “Asia’s Alternative Investments AuM To Log “Explosive” Growth – Prequin”, by Tom Burroughes, 23 Jun 2021

[17] EY, “In times of change, does accelerated adaptation present obstacles or opportunities? 2020 Global Alternative Fund Survey”, Nov 2020

[18] BCG, BCG Global Wealth Report 2021 data in “When Clients Take the Lead – Global Wealth Survey 2021”, Jun 2021

[19] EY, “In times of change, does accelerated adaptation present obstacles or opportunities? 2020 Global Alternative Fund Survey”, Nov 2020

[20] Bite Investments, “Private Equity: A Growing Opportunity for HNW Investors”, Feb 2021

[21] The Motley Fool, EY 2021 data in “81% of Ultra-High-Net-Worth Individuals Use Alternative Investments”, by Jack Caporal, 18 Aug 2021

[22] EY, “In times of change, does accelerated adaptation present obstacles or opportunities? 2020 Global Alternative Fund Survey”, Nov 2020

[23] BCG, “When Clients Take the Lead – Global Wealth Survey 2021”, Jun 2021