The Covid-induced market corrections in 2020 prompted many existing and new investors to double down on public markets – but, whilst their efforts were often handsomely rewarded, public markets are now at or near their all-time highs, with many public stocks (and bonds) selling at elevated valuations.[6]

As private wealth continues to grow, with more younger investors, female investors, emerging-market entrepreneurs, and a host of other new investors entering the investment market, those outsized returns are becoming harder to generate, and even in the best of times, buying opportunities during market corrections, such as those seen in 2020, are not sustainable long-term.[7]

Additionally, frustration with traditional asset classes is exacerbated by volatility in public markets that is now baked-in, with shares rising and falling on news bites, rumours, and minor fluctuations in overall economic conditions. These combined factors make it doubly hard for smaller investors to create long-term value, as the time-consuming tasks of persistent vigilance and acute market timing are now required to achieve the best results.

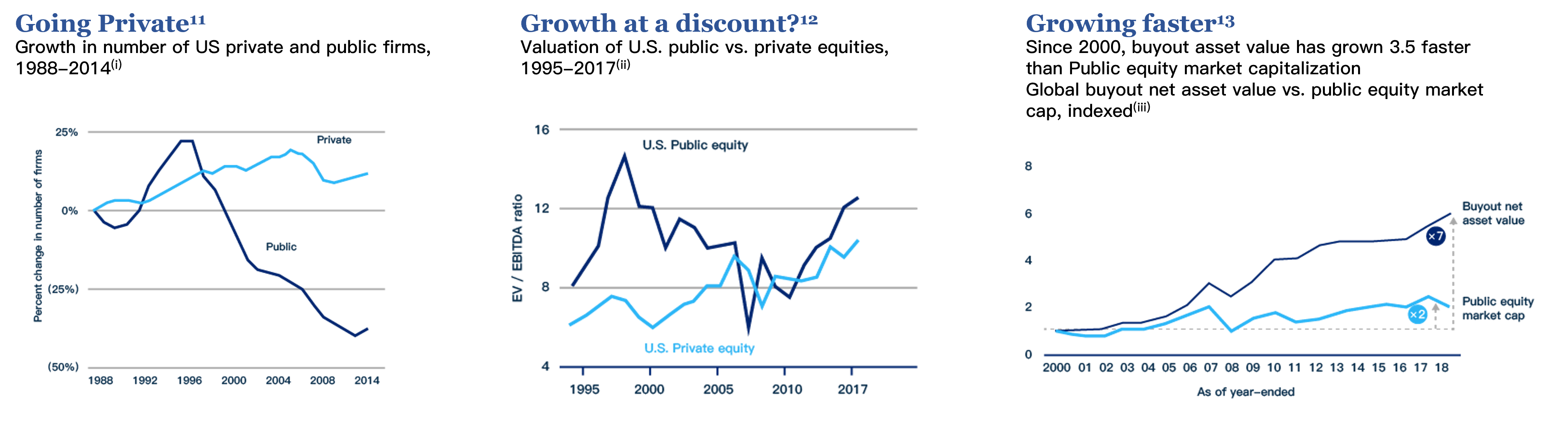

Conversely, the non-public (i.e. non-traded) nature of alternative investments allows for volatility to remain relatively subdued. The private equity market is estimated to reach US$5.8T by 2025 and it has shown great resilience to recent downturns, including the Great Financial Crisis of 2007-09 and the Covid-19 pandemic of 2020-21.[8] The American Investment Council’s Public Pension study report of 2019 indicated that private equity continues to lead all asset classes in long-term investment performance, with private equity’s median 10-year annualized net return of 10.2% outperforming public stocks at 8.5%.[9]

In addition, historically, private markets’ highest returning vintage years tend to follow recessionary periods, particularly when selecting the top managers, who can deploy capital fast and opportunistically. [10]

Finally, tomorrow’s unicorns may never go to IPO. Private companies are staying private longer and growing faster at lower valuations. Their eventual success may not be accessible via public markets. This means that investors who ignore private markets now may be limiting their portfolio’s growth potential.

(i ) Lines show the percentage change in the number of private and public firms in the U.S. since 1988.

(ii) U.S. public equity valuation exclude financials and are based on the capital IQ database of U.S. stocks. Private equity valuations are based on an annual average of leveraged buyout purchase prices and are net of fees. EV/EBITDA is a valuation metric determined by dividing a company’s enterprise value (EV) by its earning before interest, taxes, depreciation and amortization (EBITDA).

(iii) Buyout net asset value based on unrealized value.

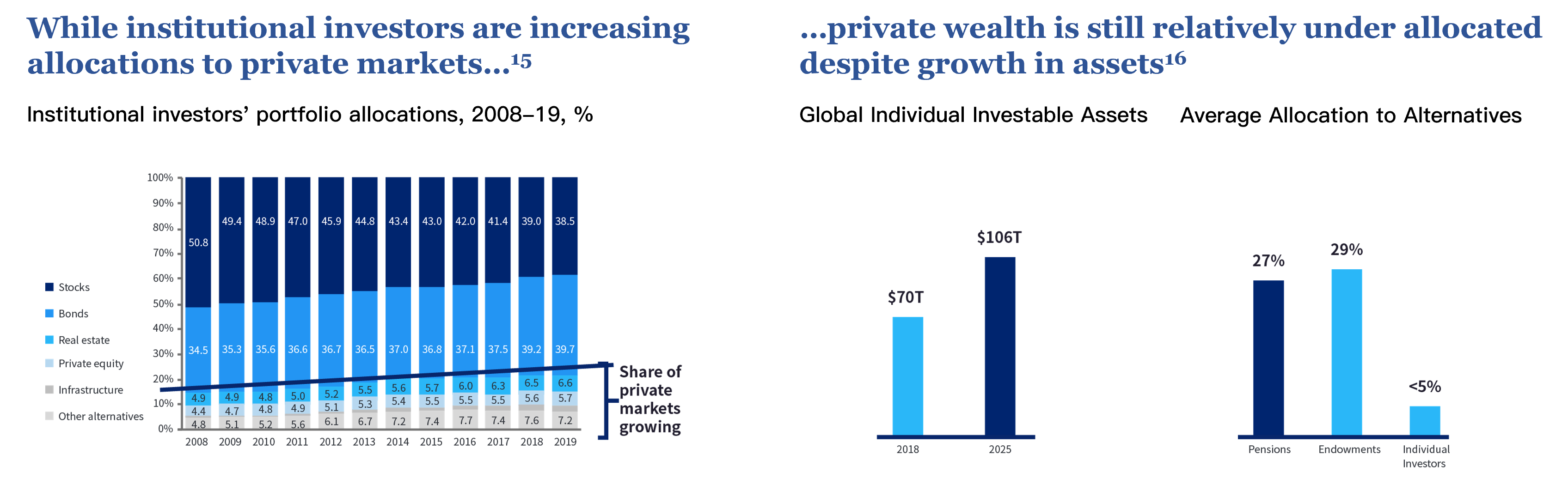

Even though global individual investable assets are predicted to expand from US$70T in 2018 to US$106T by 2025, private wealth remains under-allocated to private markets compared to institutions.

The reasons for this disparity are three-fold:

- Firstly, due to the illiquidity, longer lock-in periods, and limited opportunities to exit, private market investments are more complicated than public markets. Regulations are in place to ensure only accredited investors enter these markets.

- Secondly, specialised skills are needed to understand complex documentation, conduct due diligence, select the best performing managers, and then gain access to them. Institutional investors have historically built large teams to perform this time-consuming and expensive work, but it has typically been beyond the capabilities of individuals and even smaller family offices and wealth managers.

- In addition, the same due diligence, KYC, anti-money laundering and other regulatory checks apply to small and large investors alike. This means the admin burden on private markets managers and private banks is the same, regardless of whether the investor is investing $100k, $1million or $100million. This has made it economically challenging to accept smaller investors and has driven managers to set minimum investment sizes, often in the range of $10-20million.

Simply put, high entry costs, due diligence requirements and regulatory hurdles have long kept private markets out of reach to private wealth. It is only recently that more agile managers have stepped forward to leverage technology to remove these hurdles and create access with lower entry tickets, easy-to-understand investment data and regulatory support to satisfy investor needs.

When it comes to portfolio construction, each investor will have unique return expectations, risk tolerances, liquidity needs and investment capabilities. That said, successful investment programmes of the best institutional investors have been shown to have the following characteristics:

- Looking for and having the ability to access the top-tier funds – while past performance does not guarantee future results, top performing funds have been shown to persistently outperform public markets significantly

- Fully diversifying across the investment matrix – strategies, geographies, sectors, manager types and sizes. Exposure to risk is typically mitigated by the selection of complimentary investments – higher risk, such as venture capital, may be offset by lower risk, such as private credit or real estate. Note that this balancing act may correlate with the level of expected return – higher risk potentially coming with higher return and vice-versa.

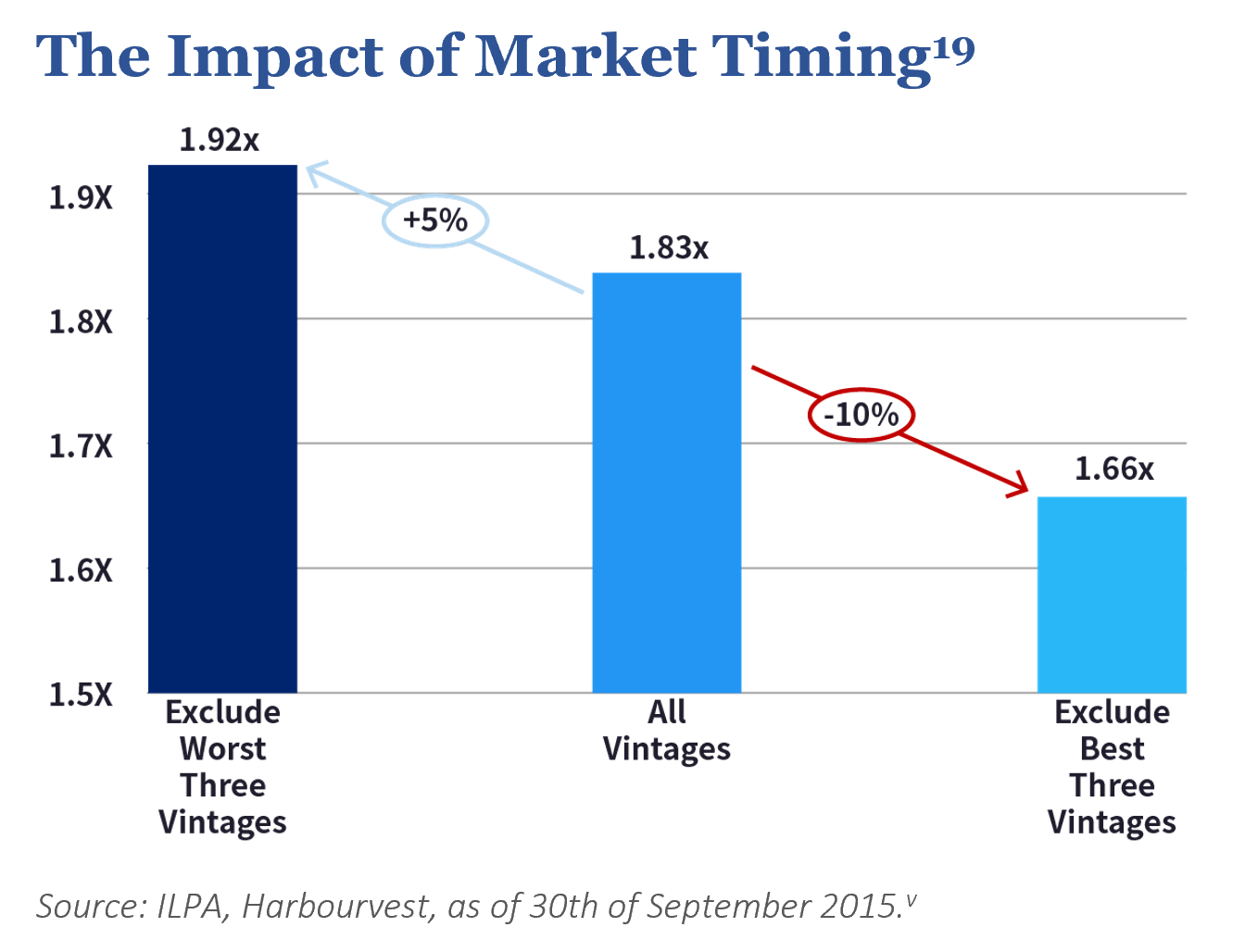

- Deploying consistently over an extended period – avoiding concentrations into high or low performance years and attempting to create balance and consistency. Most portfolios will contain assets of widely differing vintage years and exit timing. A veritable galaxy of external factors can make some vintage years better than others – this includes the state of the economy, public and private market environments, and conditions within a particular industry – but there will always be a continual exodus of investments as funds retire. Well-maintained portfolios will replace these retiring investments with new ones without pause, to retain an elevated level of consistency. However, some investors may attempt to time the market to achieve better results, opting to wait out the period between exit and new entry. Research shows that uneven investing has been shown to achieve lower returns than staying invested regardless of economic conditions.[18]

(v) Includes all HarbourVest fund/account primary partnership commitment gross returns from 1992 – 2011. Past performance is no guarantee of future returns.

Although it is impossible to guarantee what the investment and exit environments will be like over the extended life cycle of a typical private equity fund, the data reveals that outperformance in private equity is persistent and that top performers remain top performers regardless of general market conditions.

Investors seeking optimal returns should therefore take the time to research and select the best fund managers for their individual and long-term investment goals.

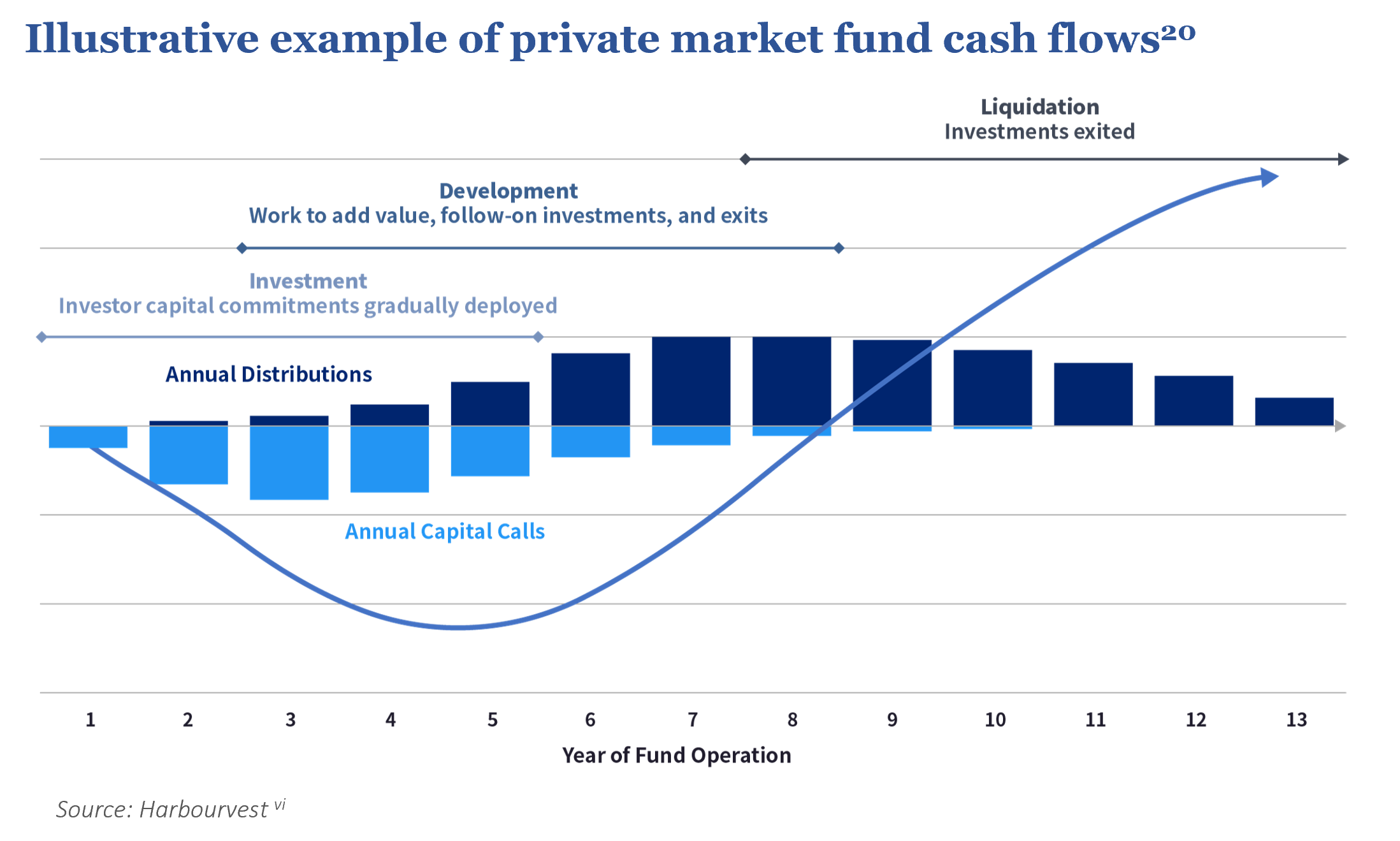

Private market investment horizons are usually longer-term.

On average, funds take 4-5 years to invest the fund, i.e., find, conduct diligence, and buy suitable portfolio companies, and then each portfolio company is held for 3-5 years, with improvements and value creation initiatives carried out before the company is sold. As such, it can take 3-5 years before investors receive their first distributions, with the bulk of distributions coming in years 5-7, and the tail-end of distributions following in years 8-10.

To fund this process, investors in private market funds agree to “commit capital”, which is effectively the total investment amount throughout the life of a fund. Investors are legally obliged to wire this money when requested by the manager. As managers identify and sign agreements to purchase companies, investor commitments are drawn down (i.e., cash is requested) on an as-needed basis to fund the company purchases, pay management fees and other expenses. The fund manager typically gives investors 7-10 days’ notice of a drawdown. Investors total commitment is drawn over years, as opposed to at once. However, investor withdrawals are not possible, so a careful consideration of liquidity requirements is advisable.

The fund managers will aim to maximize returns for investors by carrying out the improvements in the purchased portfolio companies. This can be both operational improvements, as well as an acquisition strategy to grow the businesses. As investments mature and the value creation plan is executed, the fund manager will look to ‘exit’, i.e., either sell the business to a strategic or financial buyer, or even IPO (i.e. sell the stock to the public markets). Investors then receive their share of the net proceeds pro-rata to their investment.

As the chart below shows, in the early years management fees and capital calls are made to fund company purchases. It is then followed by potential distributions in later years as value creation plans are realised, and thus, investor cash flows tend to be negative in the early years of a fund and turn positive later in the fund life as underlying investments are sold – this is called the J-curve effect.

(vi) This example is shown for illustrative purposes only and is intended to demonstrate the mechanics and cash flows of a private equity fund. It is not intended to predict the performance or cash flows of any specific fund and should not be construed as predicting the future. The actual pace and timing of cash flows of a private equity fund are highly dependent on the fund’s investment pace, the types of investments made by the fund, and market conditions. Private equity investing involves significant risks, including loss of the entire investment.

That said, investors wishing to enjoy returns from private capital investment, but who do not have the desire to wait many years to receive them, may consider a secondary investment structure. This allows investors to buy an interest in a previously raised fund, and it occurs when a third-party investor sells or exits all or a portion of their fund commitment prior to the normal liquidation period of the fund.

This practice has the triple benefit of allowing prospective buyers to gain greater visibility of the underlying portfolio companies, possibly buy-in at discount, and secure any returns sooner, as the underlying assets are typically more mature and closer to realisation.